The fund-of-funds universe is a well-established one, with around £150 billion of assets under management. These funds are popular with investors looking for a one-stop investment solution, rather than building and balancing their own portfolio. But where are these funds investing their money, and are they doing a good job?

Critics argue that fund-of-funds can erode returns for the investor as fees are typically higher than standard funds – remember you’re effectively paying the fund manager fee, and then the fee of the other funds in which he invests. Other weaknesses, says Morningstar analyst Bhavik Parekh, can include over-diversification and a lack of control over asset allocation as the fund manager is one step removed. There is also the fact that even an experienced manager can still make poor fund selection decisions.

Let’s Look at Fees

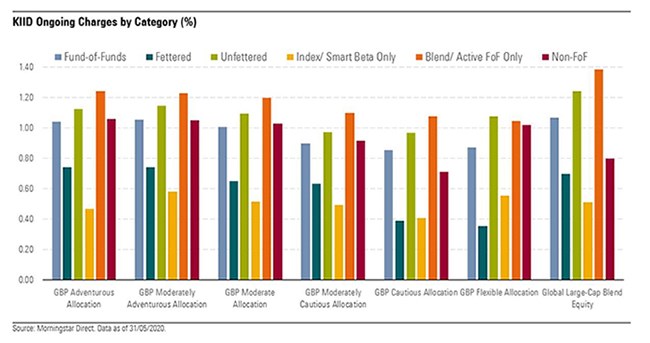

The double-layer nature of fees on fund-of-funds means they can be expensive. However, they may not be as pricey as investors expect, particularly as many of these funds now employ the use of cheap tracker funds to keep their costs down. Morningstar analysis shows that fund-of-funds typically cost more or less the same as their standard counterparts. The only category where fund-of-funds were considerably more expensive was the Morningstar global large-cap blend equity category, where they were around 27 basis points more expensive.

Funds investing in only their in-house range of funds (known as fettered funds) or in tracker funds charged on average 0.55%, while those investing in active funds from other groups charge an average of 1.14%. The averaged fettered fund is 43 basis points cheaper than the average unfettered fund – it make not sound a lot, but over time the overall effect on returns can be huge. The below chart shows the average charges of different types of fund-of-fund across five Morningstar categories.

What about Performance?

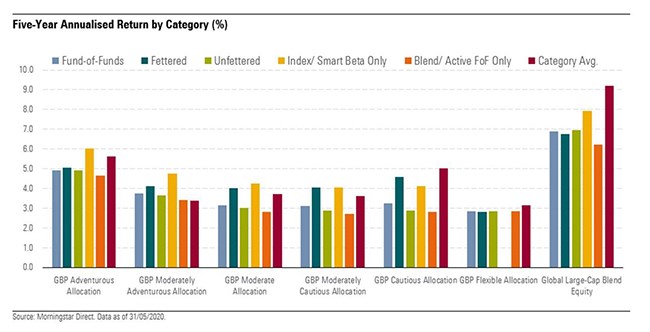

So what does all this mean for performance? The higher the fees on a fund, the greater the returns it needs to deliver to keep up with its peers. Parekh found that those fund-of-funds investing in other active funds do tend to underperform compared with standard funds, or even with fettered fund-of-funds or those focusing on passive investments. This can be seen in the chart below.

Of course, risk or volatility must also be considered, and on a risk-adjusted basis, fund-of-funds perform much better than peers in the same category. In particular, funds with a lower weighting to equities (GBP moderate allocation, GBP moderately cautious allocation, GBP cautious allocation), fared much better on a risk-adjusted basis. Even some of the fund-of-funds investing in active vehicles outperformed in these categories when measured this way.

Those with a higher weighting to equities (GBP adventurous allocation and GBP moderately adventurous allocation), meanwhile, had risk-adjusted performance that was much closer to the average. In the case of the GBP moderately adventurous allocation category, most fund-of-funds underperformed.

The implication of these results is that fund-of-funds managers are perhaps more successful in controlling risks on the downside and in delivering attractive returns.

Parekh adds: “There is an immediate cost advantage that comes with fettered funds as they will usually be charged either a zero or very low fee by the internal fund in which they are investing, which helps to keep the overall cost down. Beyond the cost advantage, in-house investments may also be better understood by the fund-of-fund manager and he will have full transparency on the underlying holdings.”

However, he also points out that the diversification benefits are somewhat limited in a fettered fund as the fund group may not have a product range that can cater for the managers' every need. The manager may also be limited if there is a “house style” across the firm’s range.

Are Fund-of-Funds Popular?

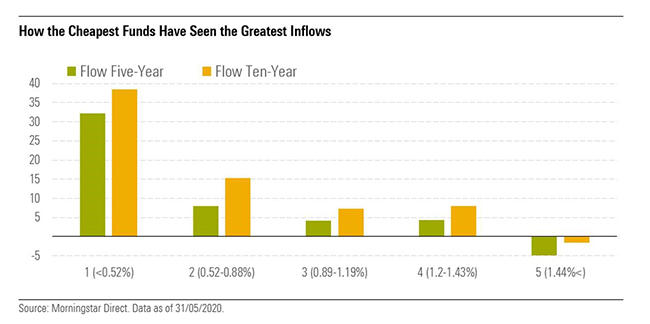

Over the past five years, fund-of-funds have attracted more than £44 billion of investors’ money. Of this, some £27 billion was invested into fettered funds, and most notably the Morningstar Analyst Gold-rated Vanguard LifeStrategy range, which has seen total net inflows of £16.4 billion over that period.

Vanguard’s has been the most popular range mainly due to its very low fees, currently 0.22%, which places it amongst the lowest cost funds-of-funds available. This follows a general investment trend of recent years, whereby funds which charge the lowest fees have tended to attract the most assets. Indeed, the below chart shows how the most expensive funds (those charging 1.44% or more) have seen outflows, while the cheapest (charging 0.52% of less) have seen the greatest inflows over both five and 10 years.

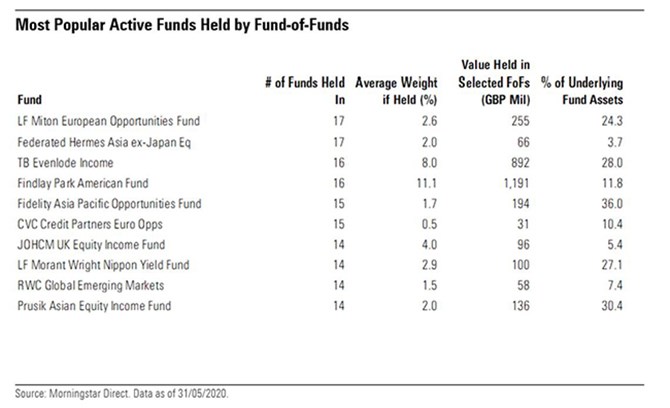

What do Fund-of-Funds Invest in?

Looking at the underlying holdings of fund-of-funds tells us where the professionals are investing their assets. Parekh looked at fund ranges with at least £1 billion of assets under management, and their holdings as of the end of Q1 2020.

iShares and Vanguard dominate the list of most popular passive options held in fund-of-funds. Of course, their popularity is helped by the fact that the two firm’s tracker funds are held by their own fund-of-funds. Indeed, around half the assets in the Vanguard FTSE Developed World ex-UK Index come from the five funds in Vanguard’s LifeStrategy range.

iShares is more popular if we consider the number of fund-of-funds in which an index fund is held. The iShares UK Equity Index fund, for example, features in 34 different fund portfolios, and iShares Japan Equity Index in 32.

Among the most popular active funds are Findlay Park American and Evenlode Income. Around 28% of the Evenlode fund’s assets come from the fund-of-funds analysed. Other funds have as much as 40% of their assets coming through fund-of-funds, and Allianz Strategic Bond a massive 47%.

While many investors may assume that fund-of-funds are more expensive and perform poorly, Parekh’s analysis shows that this is not always the case.

Fund-of-funds investing solely in active funds and which are unfettered may struggle to deliver, but the evolution of this space is bringing greater levels of success. The growing use of passive funds, for example, keeps costs down which in turn helps boost performance after fees. Parekh adds: “Performance of fund-of-funds on a risk-adjusted basis also comes out in a far better light, with many outperforming the broader market when overall risks are considered.”

An increasing focus by investors on fees has seen a flood of money into the cheapest fund-of-funds over the past five years, too. “Fees at less than 0.5% may be unrealistic for unfettered, active fund-of-funds, but by being more aggressive with negotiating fees and having a willingness to reduce margins, fees can come down for the most expensive fund-of-funds,” says Parekh. “This could potentially help to turn the tide and see more fund-of-funds enjoy the inflows seen by the cheapest products.”